—— Legislations and regulations provide investors a solid foundation for investment safety and long-term benefits. In this article, we use both English and Chinese to briefly introduce the progress of real estate-related investment and securitization in the United States and introduce JOBS Act, the legal framework of private equity funds issued by CrowdFunz, and its associated investor qualifications.

Legal Basis of Small Private Equity Offerings

The offerings of CrowdFunz private equity funds have been benefited from the development and evolution of the laws related to real estate investment in the United States over the past century.

JOBS Act (also known as Jumpstart Our Business Startups Act) enacted in 2012 dramatically accelerates the small funding sector in the real estate industry, allowing more “crowdfunding” type of funds open access to retail investors. Current available private equity funds offering on CrowdFunz are based on Jobs Act as the compliance framework, following securities laws and regulations of the United States for issuance, sales, and management.

CrowdFunz believes that a reliable investment platform can succeed only if it obeys principles of business ethics and standardized operations, and based on the above, we offer and improve our fiduciary duties and investor services.

The US Congress passed the Jobs Act in 2012 and sent the bill to President Obama

The offering amount of securities issued through the Jobs Act has surpassed that of traditional IPOs. After many amendments, the bill is now dubbed “Jobs Act 3.0”. Its continuous revisions also reflect the modernization of the US securities industry.

The Evolution of Securities Laws

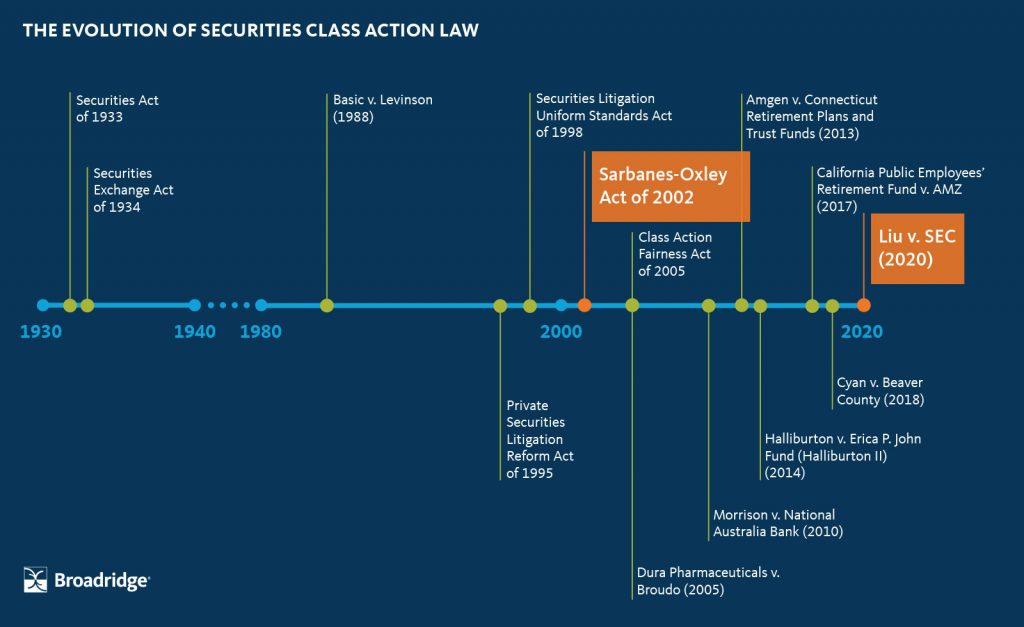

1930’s – Securities Act of 1933 & Securities Exchange Act of 1934

After the Great Depression, the United States Congress passed the famous “Securities Act of 1933” and “Securities Exchange Act of 1934”.

These two bills are the cornerstones of the modern securities industry and capital market in the United States, requiring security issuers to disclose detailed information of the offering entity, such as financial statements, asset status, changes in critical shareholders, etc.; securities offering procedures have also been further standardized.

For improving industrial integrity, issuers and third-party agencies must ensure the accuracy and trustworthiness of the disclosed information to protect the rights and interests of securities investors. Due diligence, retail investor, institutional investor, and accredited investor, those definitions widely used in the modern U.S. securities industry, all began with these two bills.

The Securities Act of 1933 was enacted by the US Congress in 1933 and was signed by President Roosevelt

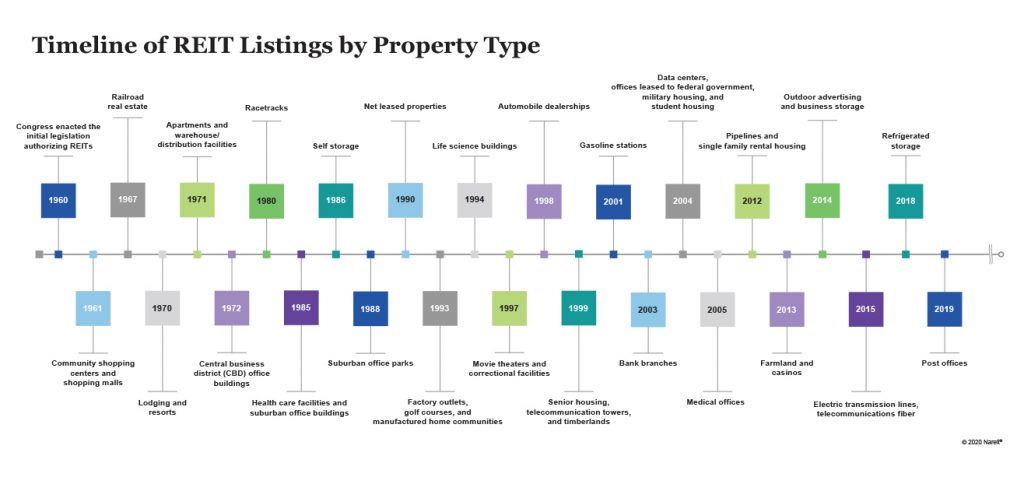

1960’s – REITs Acts

Nowadays, Real Estate Investment Trusts have become one of the most popular methods for real estate asset securitization in the United States. On September 14, 1960, U.S. Congress passed the bills to create the security category of Real estate investment trusts (REITs). After that, companies that own real estate or intend to invest in real estate can raise funds from investors through REITs, enhancing the financing capabilities of real estate projects on one hand and enabling retail investors to participate in the real estate market without huge capital investment.

Since REITs investors actually own securities, they do not need to bear the burden of real property’s illiquidity, and REITs securities can be traded in the secondary markets, which greatly increases the liquidity of the investment.

U.S. REITs continue to innovate

1980’s – Regulation A Securities Offering

Nowadays, Real Estate Investment Trusts have become one of the most popular methods for real estate asset securitization in the United States. On September 14, 1960, U.S. Congress passed the bills to create the security category of Real estate investment trusts (REITs).

According to the Regulation A of the Securities Act of 1933, companies that issue securities of less than $100,000 dollars within 12 months can be exempted from registration with the U.S. Securities and Exchange Commission, but the issuers still need to submit certain materials to the Securities and Exchange Commission. issuers that are approved and exempt from registration must still meet the requirements of the Blue Sky Laws in their offering states.

The exemption from registration from Regulation A facilitates the financing of U.S. mall and medium-sized businesses through the issuance of compliant securities. Starting from the earliest $100,000 limitation, after several amendments, in the 1980s, the offering limitation had risen to $5 million.

Important U.S. securities regulations often appear after economic crises

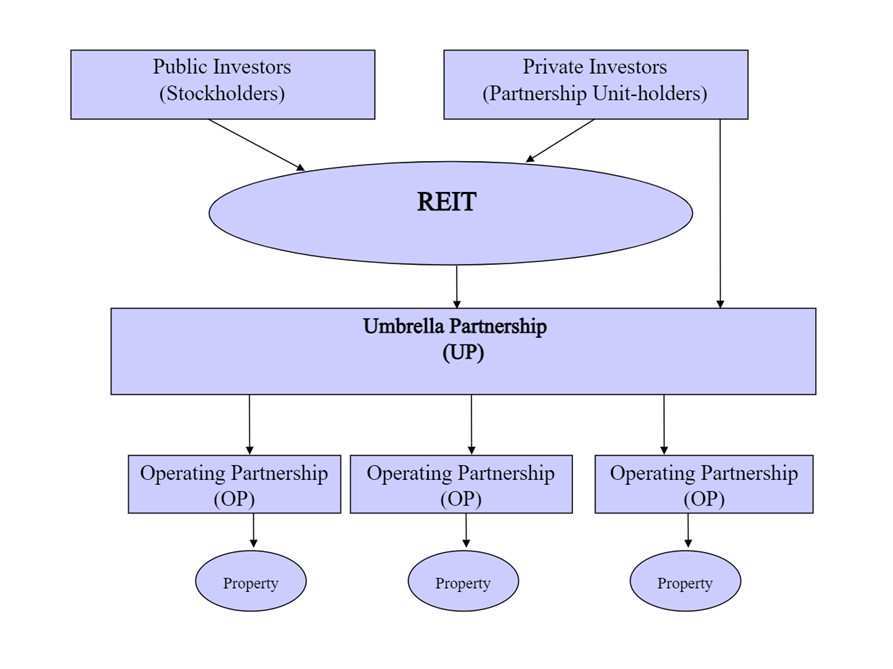

伞状合伙制REIT促进了私募投资机构使用该金融工具

1990’s – REITs Modernization

In 1992, the Umbrella Partnership Real Estate Investment Trusts (UPREITs) appeared in the U.S. capital market. This type of new REIT not only allows investors to obtain tax incentives but allows fund managers to obtain the flexibility to operate and manage their real estate, which further improves the REITs securitization and absorbs more large private equity firms to participate in REITs.

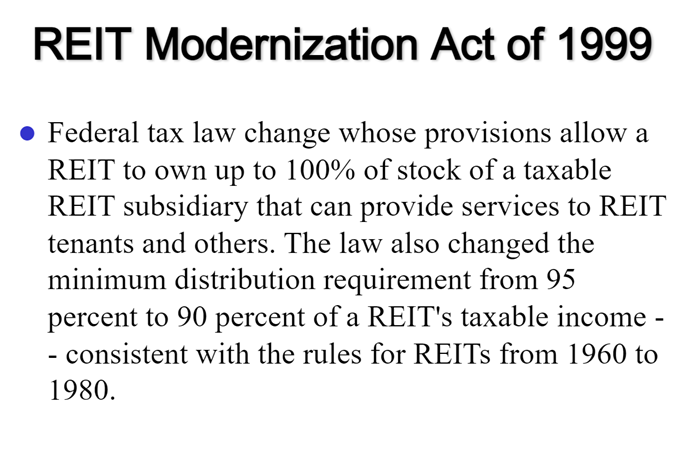

In addition, the Taxpayer Relief Act of 1997 and the REIT Modernization Act of 1999 were successively passed in the United States, allowing REIT to enjoy more tax relief benefits, enhancing the competitiveness of REITs in the capital markets.

The REITs Modernization Act of 1999 increased the attractiveness of this financial instrument at the level of federal tax law

2010’s – Jumpstart Our Business Startups Act

With the years’ efforts of all parties, former U.S. President Barack Obama signed and promulgated the JOBS Act (Jumpstart Our Business Startups Act) in April 2012 and amended it in October 2015. This historic bill aims to provide convenient financing channels for small-and-medium enterprises after the 2008 financial crisis, thereby increasing employment opportunities and promoting economic growth in the United States.

Like CrowdFunz, the U.S. real estate crowdfunding platforms could participate in the real estate investment field in the form of small private equity funds in accordance with JOBS Act. Moreover, as a part of JOBS Act, the amended Regulation D, and Regulation A exemption offerings are now inputting the largest capital amount into the U.S. real estate industry.

In 2012, President Obama formally signed the JOBS Act at the White House

Investor Qualifications for Private Equity

The private equity funds offered on CrowdFunz platform are all in compliance with Title II of JOBS Act and Rule 506(c) of securities law.

The U.S. Securities Exchange Committee allows Rule 506(c) offerings to do general solicitation and to sell its securities to accredited investors through internet. The offerings and sales of the securities do not require the issuer to hold a Broker-Dealer license in FINRA system.

In Title II of JOBS Act, to invest Rule 506(c) offering securities, an investor must be identified as an Accredited Investor in conformity with at least one category listed below:

- The investor’s personal net worth or family net worth with his spouse exceeds $1 million (excluding real property used for self-occupation);

- In the past two years, the investor’s annual income has exceeded $200,000, and the investor’s annual income will also maintain the same level in this fiscal year;

- In the past two years, the combined annual income of the investor and his spouse has exceeded $300,000, and the combined annual income will also maintain the same level in this fiscal year.

The word Accredited investor is a term used in Rule 501 of Regulation D in the United States securities law. Accredited investor shall mean any person who comes within any of the following categories, or who the issuer reasonably believes comes within any of the following categories, at the time of the sale of the securities to that person:

- Any bank as defined in section 3(a)(2) of the Act, or any savings and loan association or other institution as defined in section 3(a)(5)(A) of the Act whether acting in its individual or fiduciary capacity; any broker or dealer registered pursuant to section 15 of the Securities Exchange Act of 1934; any investment adviser registered pursuant to section 203 of the Investment Advisers Act of 1940 or registered pursuant to the laws of a state; any investment adviser relying on the exemption from registering with the Commission under section 203(l) or (m) of the Investment Advisers Act of 1940; any insurance company as defined in section 2(a)(13) of the Act; any investment company registered under the Investment Company Act of 1940 or a business development company as defined in section 2(a)(48) of that act; any Small Business Investment Company licensed by the U.S. Small Business Administration under section 301(c) or (d) of the Small Business Investment Act of 1958; any Rural Business Investment Company as defined in section 384A of the Consolidated Farm and Rural Development Act; any plan established and maintained by a state, its political subdivisions, or any agency or instrumentality of a state or its political subdivisions, for the benefit of its employees, if such plan has total assets in excess of $5,000,000; any employee benefit plan within the meaning of the Employee Retirement Income Security Act of 1974 if the investment decision is made by a plan fiduciary, as defined in section 3(21) of such act, which is either a bank, savings and loan association, insurance company, or registered investment adviser, or if the employee benefit plan has total assets in excess of $5,000,000 or, if a self-directed plan, with investment decisions made solely by persons that are accredited investors;

- Any private business development company as defined in section 202(a)(22) of the Investment Advisers Act of 1940;

- Any organization described in section 501(c)(3) of the Internal Revenue Code, corporation, Massachusetts or similar business trust, partnership, or limited liability company, not formed for the specific purpose of acquiring the securities offered, with total assets in excess of $5,000,000;

- Any director, executive officer, or general partner of the issuer of the securities being offered or sold, or any director, executive officer, or general partner of a general partner of that issuer;

- Any natural person whose individual net worth, or joint net worth with that person’s spouse or spousal equivalent, exceeds $1,000,000;

- Any natural person who had an individual income in excess of $200,000 in each of the two most recent years or joint income with that person’s spouse or spousal equivalent in excess of $300,000 in each of those years and has a reasonable expectation of reaching the same income level in the current year;

- Any legal entity in which all of the equity owners are accredited investors;

The private real estate fund products offered on CrowdFunz platform are designed for the U.S. accredited investors in the above definition.

At the same time, the U.S. Securities Law also has Regulation S for non-U.S. investors. In Regulation S, if a U.S. entity issuance occurs outside the U.S., the issuance is no longer subject to U.S. Securities laws and does not require mandatory information disclosure. The offerings pursuant to Regulation S also allow foreign investors to purchase the securities without the qualification of the above-mentioned accredited investors.

In other words, for Chinese investors, benefiting from the exemption provided by Regulation S, they can invest such private equity funds without the qualification of accredited investors and be feasible to subscribe to the fund products listed on CrowdFunz platform.

Summary

In U.S. capital markets, the securitization of real estate investment is based on relevant laws and regulations that have more than 50 years of history. In the case of JOBS Act, the legislation lasted for three years and experienced several steps, involving industrial and legal discussions and amendments, and it is tailored for small and medium enterprises to reduce the burden on fundraising. Also, the legislation has created a new blue ocean in the U.S. real estate investment sector.