—— Through CrowdFunz’s funds, investors have the opportunity to invest in different types of U.S. real estate investment types. Understanding the characteristics of each strategy will help investors choose corresponding funds that suit investor demands based on risks and expected returns.

There are many ways to classify real estate investment types in the United States. One of them is to classify investment strategies based on the level of risk-return trade-off.

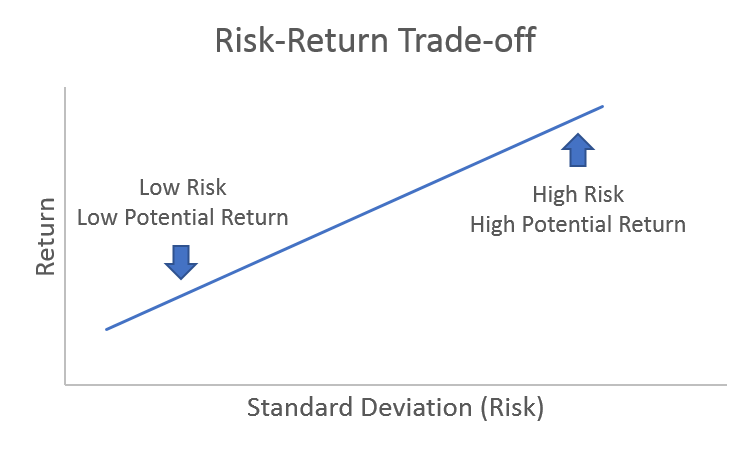

The risk-return trade-off is the cornerstone to understand the investment

Investors are compensated by the risk level that they are bearing.

Real estate investment has one thing in common with investment in other types of assets in the capital market, that is, the actual return obtained by investors is often consistent with the risks they bear during the investment period.

Therefore, investment with low risk will never provide a high rate of return, and investment with a low rate of return will not bring higher risks.

Of course, the above concept of investment must also be based on the trustworthiness and transparency of fund management and sales.

In addition, the higher the risk-return level, the higher the uncertainty of investment. It is called Risk Exposure. The higher the uncertainty, the bigger the risk exposure.

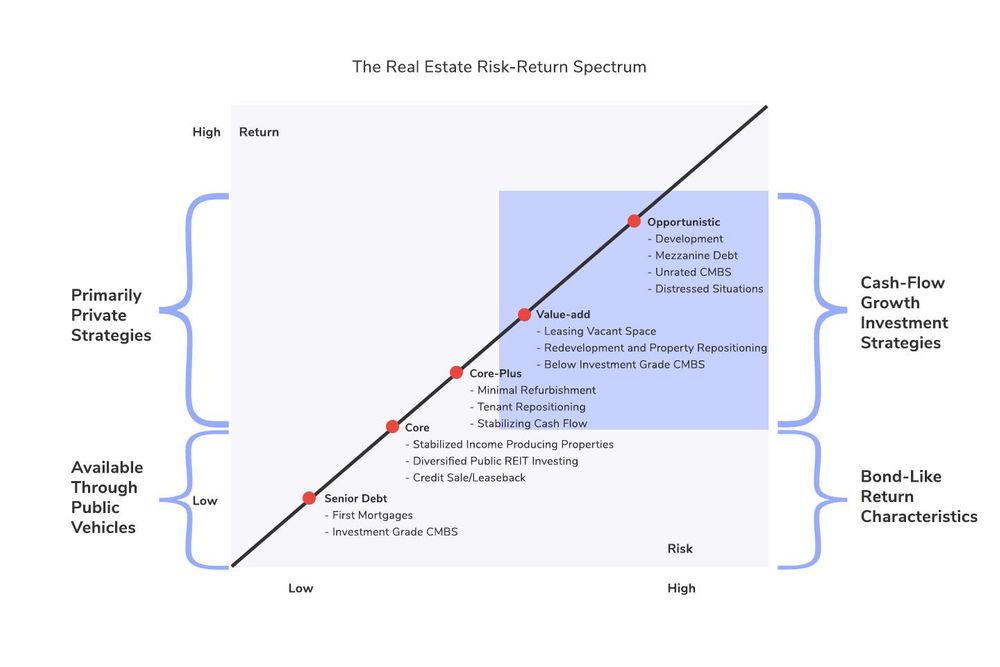

Different real estate investment strategies have different risk-return trade-offs

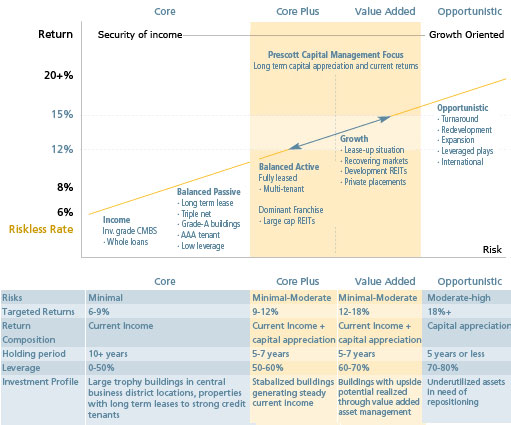

According to the level of risk-return trade-off, real estate investment strategies are mainly classified into the following four types:

- Core: low risk/low return;

- Core Plus: relative low risk/low return;

- Value Added: Medium to high risk/medium to high return;

- Opportunistic: high risk/high return.

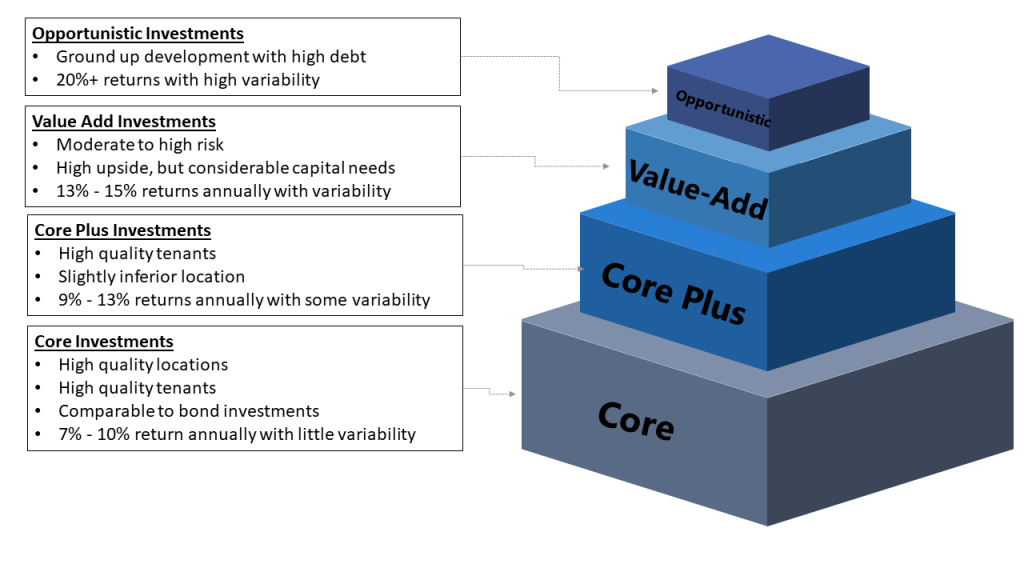

Core strategy

The core investment strategy often refers to the strategy of holding real estate with stable prices and cash flows for a long time

After purchasing real estate, investors can obtain continuous income through stable cash flow.

The underlying real estate of this type of investment is mainly concentrated in the core areas of metropolitan regions, such as the prosperous areas of cities like New York and Los Angeles. The type of real estate is often commercial properties such as office buildings, retail spaces, shopping malls, or residential properties such as leasing apartments and student housing. The tenants of these properties are usually long-term tenants with good credit backgrounds.

The core investment strategy has relatively low risk. It focuses on the ability of assets to continuously generate cash flows, rather than the ability of asset appreciation during the period from purchase to disposal.

The core strategy is characterized by low risk and low return.

Core-plus strategy

The core-plus investment strategy is similar to the core strategy, but the property locations are not so popular (located in the surrounding markets of small cities or metropolises), leasing terms are relatively shorter, and the status of the property may require renovation.

Those reasons create more risks than the core type, so the return on investment is higher than that of the core strategy. Also, part of the capital invested will be used to improve or increase the value of assets.

In the more mature real estate markets like Europe and the United States, as the commercial real estate (CRE) market is relatively well-developed, there are much more core and core-plus investment opportunities than in China.

The core-plus strategy is featured by its moderate risk-and-return trade-off.

Value-added strategy

Investors with value-added investment strategies generally purchase real estate when the price is low, renovate the building, change marketing, and lease strategies to increase the value of the asset. After holding it for a medium to long-term period, the price will be higher. Sell real estate to get capital gains, or continue to hold real estate to get a higher capital rate (Cap Rate) cash flow.

Different from the core and core-plus investment strategies, the capital required for real estate renovation and asset appreciation for value-added strategies account for a higher proportion of the total capital invested, and the rental or sale activities need to wait until the relevant project constructions are completed. Only after that can it officially start.

Therefore, investors with value-added strategies often use higher leverage to help them successfully pass the transition period for renovation and asset appreciation preparations.

For the entire real estate project invested by a general value-added strategy, the loan-to-value ratio will be between 40% and 70%, and the internal rate of return (IRR) of the project will be required to be above 10%.

Whether in the core locations of metropolitan areas or in the small and medium-sized markets of second and third-tier cities, there will be opportunities for value-added real estate investment, but generally speaking, the risk-return levels in the core locations of metropolitan areas are relatively low, while the risk-return levels in the small and medium-sized markets are relatively high.

The core strategy has its feature of medium to high risk-return trade-off. Underlying properties need to be renovated or repaired to reach better conditions, which will bring additional returns through asset appreciation.

Opportunistic

Opportunistic strategies generally refer to new real estate developments starting from the acquisition of land, or development projects that require large-scale renovation of current properties, regardless of whether the final property is for commercial or residential purposes.

Compared with the other three strategies mentioned earlier, the opportunistic strategy has the greatest investment risk, because it takes longer to create cash flow after the real property is purchased, and the capital required during the entire development process is more likely to exceed the budget.

Regardless of the real estate market in the United States, new or large-scale construction of real estate projects is a huge challenge for investors and project developers. It not only requires investors to have strong financial support but also requires developers to have development experience, regional familiarity, and rigorous cost control and project management capabilities.

In fact, similar to its level of risk-return trade-off, opportunistic investment strategies imply high risks and high returns, and at the same time, investment uncertainty or risk exposure is also large. The possibility of the final result of an opportunistic strategy covers a huge range from huge losses to super high returns.