—— In recent years, Chinese companies or investors have become more and more enthusiastic about overseas investment. However, as long as there is an investment behavior, one must face tax issues related to the investment income. This article will briefly describe the tax advantages that you can enjoy when using corporate entities to invest in real estate in the United States as a foreign investor.

Entity investment mode for overseas investors

Overseas investors generally refer to non-U.S. investors who do not have legal residence status in the United States and do not need to bear corresponding taxes. The U.S. Internal Revenue Service defines this group of people as Nonresident Alien.

Overseas investors can still freely purchase real estate in the United States or make real estate-related investments.

The purchase of real estate is the most traditional real estate investment model.

In the United States, this type of investment model includes individual and joint ownership according to the form of ownership, and more generally, the use of corporate entity ownership.

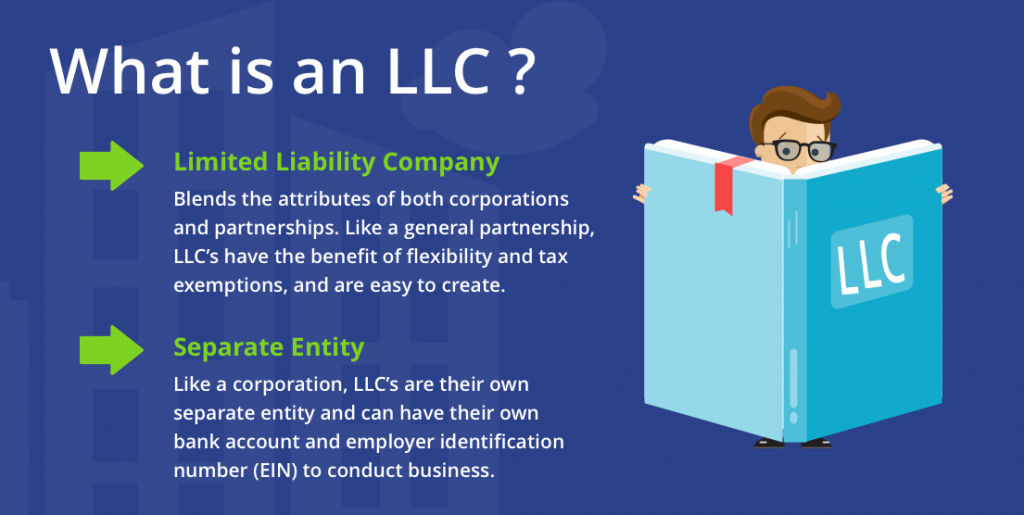

There are usually three ways to own properties in the form of a company: partnership, limited liability company, or S-Corporation.

For overseas investors, the more common way is to form a limited liability company in the United States to own or invest in real estate.

The form of investment through a limited liability company (LLC.) does not have the problem of “double taxation“, and the company has limited liabilities and does not involve personal property losses.

An individual can form a limited liability company; a family or multiple partners can also jointly form a limited liability company.

If individuals are used to investing in real estate, the rental income generated by real estate and the capital gains generated by the future sale of real estate are all in the category of personal income, so various personal taxes need to be paid.

For foreign investors, if they invest in real estate through a company, they will enjoy the preferential taxation of the company and use Form 1040-NR to file tax returns to further obtain personal-level tax exemptions.

From the perspective of the corporate legal framework, all funds available on CrowdFunz platform are all entities of limited liability company (LLC.). Therefore, if you are an overseas investor who is not a U.S. resident and invests in such funds, you will enjoy the same tax consequences.

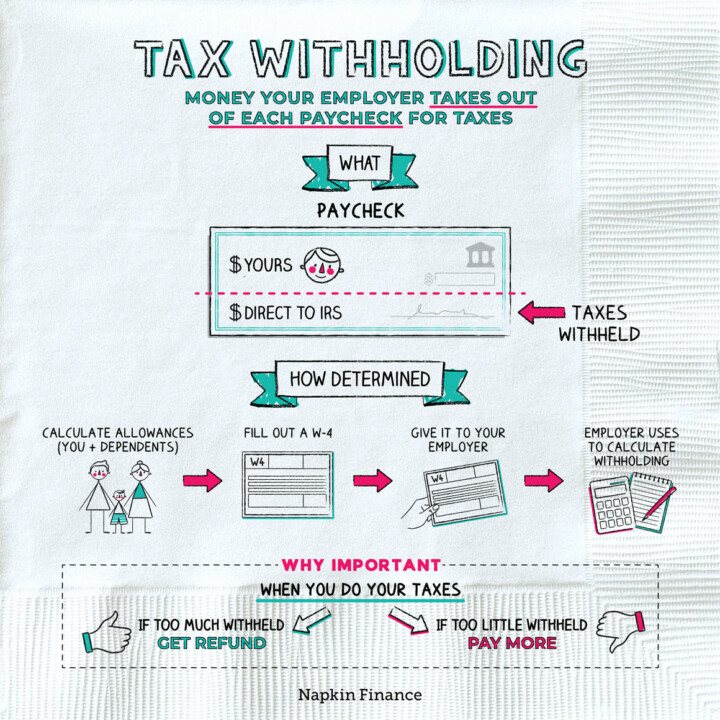

What is tax withholding

Although foreign investors can enjoy tax incentives for real estate investment through corporate entities, when overseas investors finish investments, at the personal tax level, the IRS and state taxation departments will require deposit equals to 15% of total investment returns, deducted from the returns (including dividends, principal, profit and interest), as a deposit for the next year’s tax return. This deposit is called Tax Withholding.

For example, if the sale of real property (not owner-occupied) obtains more than $300,000 cash, the seller or its agent is obliged to deduct the withholding tax on the proceeds from the sale, and the deposit will be held by IRS. The deducted amount is 15% of the real estate price, regardless of the property’s appreciation.

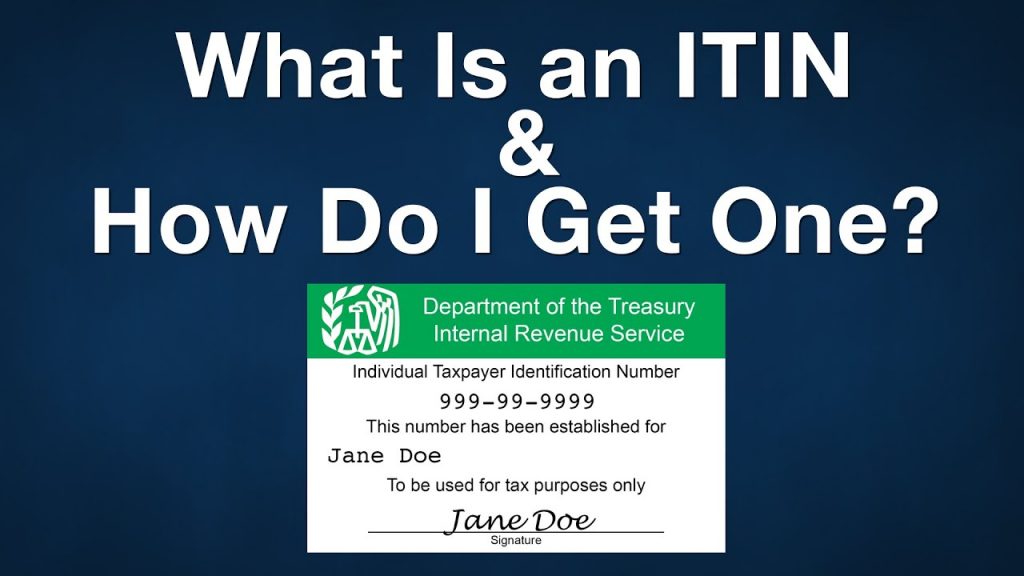

What is ITIN

Before foreign investors pay withholding taxes, investors must apply to the U.S. Internal Revenue Service (IRS) for an Individual Taxpayer Identification Number (ITIN).

The application for ITIN is one-time. For most foreign investors, it is usually when they need to declare personal federal tax before they have the qualifications and conditions to apply.

There are three ways to apply for ITIN:

- Go directly to the local office of the U.S. Internal Revenue Service. Bring your original passport, tax form for the year, and ITIN application form-referred to as Form W-7. This method is the easiest and most efficient, usually within 4-6 weeks, you will receive a reply from the IRS to complete the application.

- Mail a copy of the passport certified by the government of the individual’s nationality, tax form for the year, and Form W-7 to the IRS. It is worth mentioning that the notarization of the sent passport copy needs to be processed at the U.S. consulate in China, not the Chinese consulate in the US. Approximately 4-10 weeks after the application is sent, the applicant will receive a response from the IRS.

- Mail the original passport, tax form for the year, and Form W-7 directly to the IRS. Instead of using notarized copies of passports, applicants who adopt this method must bear the risk that their passports may be lost during the mailing process.

Since 2016, the IRS has also issued new regulations: If the ITIN that has not been used to submit federal income tax forms in the past 5 consecutive years, it will become invalid; if afterwards, taxpayers need to declare federal taxes, they must re-fill the application, active or apply for a new ITIN again.

Unexpected situations

Since non-US residents cannot be like US residents, prepaying quarterly or settle the previous year’s personal income tax at the end of the year in a lump sum, companies invested or held by non-US residents must calculate the withholding tax in advance of the previous year’s income of each foreign investor related to the company’s ownership at the highest tax rate, and pay it to the IRS and State-level tax authorities.

In this tax payment process that requires consideration of withholding tax, the following two situations may occur:

- If the corporate entity in which the foreign investor has an interest does not withhold and prepay the personal income tax related to the foreign investor’s investment in accordance with the regulations, the corporate entity shall bear the personal income tax that the foreign investor actually needs to pay;

- If the corporate entity in which the foreign investor has an interest has withheld and prepaid the foreign investor’s personal income tax in accordance with the regulations, but the investor has not declared the U.S. personal tax, the IRS may send a letter saying that you You have income every year, but the IRS does not have your tax filing records, and you need to pay the corresponding taxes.

Jason Wang, a senior CPA of New York state, provides opinions for this article. Mr Wang has been engaged in accounting business in New York for more than 20 years and is also engaged in real estate tax planning and other related fields, committed to providing professional and meticulous services to enterprises and individuals.