—— On June 24, the Brexit referendum was settled. Because it is very different from the previous market expectations, Brexit has become a black swan event, triggering violent turbulence in the global financial market. Some insiders pointed out that Chinese investors shall consider the opportunities to adjust asset allocation and increase the proportion of safe-haven assets.

Brexit amplifies market risk avoidance

On June 24th when the Brexit referendum ended, the British, French, and German stock markets all plunged about 10% when they opened.

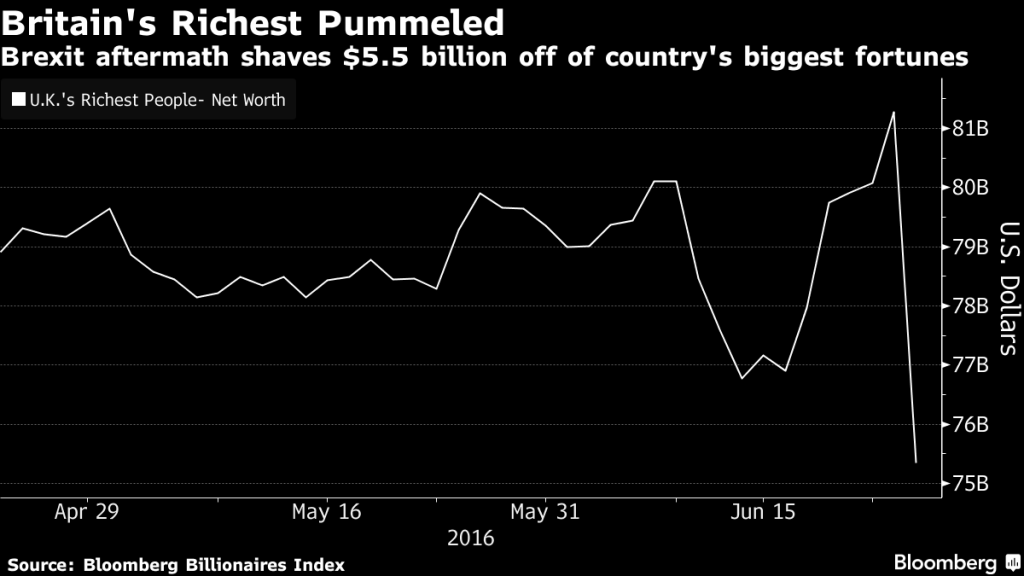

After Britain voted to leave the European Union and shocked the global market, Britain’s richest men lost $5.5 billion on Friday. According to the Bloomberg Billionaires Index, the 15 richest British people experienced sharp asset value declines. At the same time, European capital markets also suffered the largest decline since the 2008 financial crisis to its new lowest level.

After Brexit, the wealth of Britain’s richest people instantly shrank by $5.5 billion

At the same time, pound weakened to its lowest point in 30 years

Some experts pointed out that in the short term, Brexit will further amplify the risk avoidance in the market and intensify the price volatility of global investment assets.

The Brexit incident has also received attention from the Chinese financial community. Guan Qingyou, executive director of China Minsheng Securities Research, said in an interview with People’s Finance that Brexit has triggered a decline in global investors’ risk appetite, which is generally positive for safe-haven assets such as the U.S. dollar, gold, and U.S. Treasury bonds, and is negative for stocks, emerging market currencies, and crude oil. Risk assets such as Brexit will hurt both sides in the short term, which is bad for the British pound and the euro.

Zhang Qiang, the chief investment officer of Zi Lifang, has a similar view. In his view, the current global risk aversion sentiment has risen sharply, and the financial market still needs time to digest the negative factors of Brexit, the US dollar will appreciate passively, and safe-haven assets such as gold will continue to be sought after by the market in the short term. He predicted, “In the next few months, the impact of Brexit will be more pronounced. From the perspective of the Fed, the euro, pound, and risk aversion have pushed up the US dollar, and interest rate hikes are likely to be absent during the year. The Bank of Japan’s The easing policy may also continue.”

The ever-increasing overseas asset allocation requires hedging

For investors, China’s “high-yield asset shortage” is still continuing. Chinese investors are gradually adapting to the 3%-4% annualized rate of return. Taking into account the fluctuation of the RMB exchange rate, overseas investment channels have been constrained in the past. Assets and their yields are beginning to be attractive to domestic investors.

At present, China’s capital market has few investment products to choose from, and the correlation between varieties is high, making it difficult to diversify risks.

Xiao Gang, Chairman of China Securities Regulatory Commission, emphasizes the eight major directions of market reform

According to statistics, as of the end of April this year, there were 1,630 ETFs (Exchange Traded Funds) in the U.S. market covering various assets, of which 611 track global stocks and 278 track bonds.

In contrast, there are only 126 ETFs in domestic index products, and nearly 80% are tracking China’s A-share.

In developed countries such as Europe and the United States, high-net-worth clients generally have more than 10-15% of assets allocated overseas, while the proportion of overseas asset allocation by large investment institutions is higher.

As of 2016, the asset management scale of China’s financial industry is approximately RMB 93 trillion. Assuming that only 5% is allocated overseas, it is also a market of nearly RMB 5 trillion.

This year, the “China Private Banking Research 2016” jointly issued by China Industrial Bank and the Boston Consulting Group (BCG) predicts that in the next five years, the proportion of Chinese personal overseas asset allocation will rise from the current 4.8% to about 9.4%. The new market size will reach about RMB 13 trillion.

Statistics from the China Fund Industry Association show that the size of QDII public funds in 2015 has increased from RMB 48.7 billion at the end of 2014 to RMB 66.3 billion with an increase of 36%.

Summary

Brexit has led to rapid growth in global demand for safe-haven assets, of which the real estate sector is also an important underlying asset sector. The demand for overseas asset allocation of Chinese institutions is constantly increasing, waiting for the “escort” of regulatory policies to make overseas investments rationally within a stable compliance environment.

In the past year, China’s capital market has been opening up significantly faster. In the future, as the internationalization of the renminbi continues, the opening of cross-border capital accounts may become a trend. If this part of the compliance caliber is finalized, the demand that was suppressed in the past due to capital account controls will be expected to be further released.

The People’s Bank of China, the central bank of China, also made it clear in its recent 2015 annual report that the key tasks in the future include: further promoting the two-way opening of the capital market, and timely launching of the qualified domestic individual investor overseas investment system (QDII2).

CrowdFunz believes that under these big trends, real estate investment in the United States will be more favored by Chinese investment institutions and high-net-worth individuals in the future.

The data in this article comes from The Wall Street Journal, Financial Times, and Bloomberg, etc.