—— Meta Becomes Largest Nuclear Buyer with Landmark 6-Gigawatt Deal; TSMC Revenue Beats Estimates, Signaling Resilient AI Demand for 2026; Trump Directs Fannie and Freddie to Buy $200 Billion in Mortgage Bonds; China Auto Exports Set to Hit Record 7 Million as Firms Offload Surplus; Bullion Faces First Major Test of 2026 Amid $11.7 Billion Fund Rebalancing; US Housing Starts Hit Post-Pandemic Low in October Amid Data Delays; US Job Growth Slows to 50,000 in December; Unemployment Unexpectedly Dips to 4.4%

1. Meta Becomes Largest Nuclear Buyer with Landmark 6-Gigawatt Deal

Meta Platforms Inc. has secured its position as the leading corporate buyer of nuclear energy after signing a series of power agreements that could total more than 6 gigawatts. The massive procurement effort, announced Friday, dwarfs recent nuclear deals by Amazon, Alphabet, and Microsoft, signaling Meta’s aggressive push to lock in the 24/7 carbon-free power required to sustain its artificial intelligence ambitions.

The agreement includes power purchases from three existing Vistra Corp. plants and long-term support for next-generation small modular reactors (SMRs) being developed by Sam Altman-backed Oklo Inc. and Bill Gates-backed TerraPower LLC. Following the news, Vistra shares jumped 10% in pre-market trading, while Oklo surged 20%. As data centers drive a projected 30% spike in U.S. electricity demand by 2030, tech giants are increasingly turning to nuclear energy to bypass the grid bottlenecks threatening AI development.

While nuclear projects face long regulatory and construction timelines, their ability to provide consistent, high-density energy makes them the preferred choice for hyperscalers committed to both rapid AI growth and net-zero targets.

Bloomberg – Meta Signs Multi-Gigawatt Nuclear Deals for AI Data Centers

______

2. TSMC Revenue Beats Estimates, Signaling Resilient AI Demand for 2026

Taiwan Semiconductor Manufacturing Co. (TSMC) reported quarterly revenue that surpassed analyst expectations on Friday, easing fears of an artificial intelligence spending bubble. Based on monthly data, the primary foundry for Nvidia and Apple recorded revenue of NT$1.05 trillion (approximately $33.1 billion) for the quarter ending December 2025, a 20% year-over-year increase that beat the consensus estimate of NT$1.02 trillion.

[Image showing TSMC’s 2025 annual revenue performance and ASML stock record Jan 2026]

For the full year of 2025, TSMC’s consolidated revenue surged 31.6% to NT$3.81 trillion. The results reflect the sustained appetite for high-performance computing (HPC) chips used in AI data centers and robust shipments of the iPhone 17 lineup. In response to the data, shares of key equipment supplier ASML Holding NV rallied to an all-time high.

While some investors worry that the massive capital expenditures by tech giants like Microsoft and Meta—now exceeding $1 trillion collectively—may outpace actual AI software adoption, TSMC’s record numbers suggest that the hardware production pipeline remains fully booked heading into 2026.

Bloomberg – Nvidia’s Go-To Chipmaker TSMC Sees Revenue Top Estimates

______

3. Trump Directs Fannie and Freddie to Buy $200 Billion in Mortgage Bonds

President Donald Trump is directing Fannie Mae and Freddie Mac to purchase $200 billion in mortgage-backed securities (MBS), his latest intervention aimed at boosting housing affordability ahead of the November midterm elections. Announcing the move on Truth Social Thursday, Trump stated that his decision not to sell the two government-sponsored enterprises (GSEs) during his first term allowed them to amass enough cash to fund this initiative, which he claims will drive down mortgage rates and monthly payments.+1

The announcement triggered a rally in mortgage bonds relative to Treasuries and sent shares of mortgage lenders like Rocket Companies and LoanDepot soaring. Bill Pulte, Director of the Federal Housing Finance Agency (FHFA), confirmed that Fannie and Freddie have “ample liquidity” to execute the purchases quickly. While the 30-year fixed mortgage rate currently averages around 6.16%, analysts estimate this $200 billion injection could shave off another 25 to 50 basis points.

However, some economists caution that while lower rates may provide temporary relief for buyers, the move could inadvertently fuel home price inflation due to the persistent lack of housing inventory across the United States.

Bloomberg – Trump Tells Fannie, Freddie to Buy $200 Billion of Mortgage Debt

______

4. China Auto Exports Set to Hit Record 7 Million as Firms Offload Surplus

China’s automotive exports are expected to expand by as much as 25% to a record high of over 7 million units this year, according to estimates from UBS and the China Passenger Car Association (CPCA). As domestic demand for petrol cars collapses and EV growth cools, manufacturers are increasingly leveraging overseas markets as a “pressure valve” to absorb excess production capacity.

While internal combustion engine (ICE) exports are projected to rise 4% to 3.4 million units, electric vehicle shipments are forecasted to surge by more than 50% to 3.7 million units. Global giants like Volkswagen and Hyundai are repurposing their Chinese facilities to target lucrative export destinations such as Mexico, the Middle East, and Russia. UBS analysts predict that China’s total auto exports will double from 2024 levels to reach 9.4 million units by 2030.

This strategic pivot allows Chinese firms to keep plants operational rather than shutting them down, significantly intensifying competition for local manufacturers in foreign markets.

Financial Times – Chinese car exports set to jump as domestic sales cool

______

5. Bullion Faces First Major Test of 2026 Amid $11.7 Billion Fund Rebalancing

The historic rally in precious metals is facing its first significant challenge of 2026 as a wave of index fund rebalancing triggers more than $11 billion in potential selling. According to JPMorgan calculations, commodity index trackers are expected to offload approximately $6.1 billion in silver and $5.6 billion in gold during the annual rebalancing window running from January 8 to 15.

This institutional selling is a mechanistic response to the “stratospheric” gains seen in 2025, where gold climbed over 60% and silver surged more than 160%. To maintain target allocations, benchmark indices like the Bloomberg Commodity Index must trim these overweighted positions. Analysts at MKS Pamp note that while this provides a “big test” for the market’s high base, it may also create a “buy the dip” opportunity similar to early 2025, when massive buying appetite eventually overwhelmed the forced selling.

Silver is expected to endure the heaviest pressure, with projected sales equivalent to roughly 10% of the total open interest on the Comex derivatives exchange.

Financial Times – Gold and silver under scrutiny as index changes spark wave of bullion sales

______

6. US Housing Starts Hit Post-Pandemic Low in October Amid Data Delays

Housing starts in the United States plummeted in October to their lowest level since the 2020 pandemic onset, according to figures released Friday. The report was significantly delayed by the 43-day federal government shutdown (the longest in history, ending November 12, 2025), which shuttered the Census Bureau’s data collection during the critical fall period. The results confirm that builders are aggressively pulling back as they struggle with high material costs and elevated mortgage rates.

[Image showing US Single-Family vs Multi-Family housing starts comparison October 2025]

New residential construction decreased 4.6% to an annualized rate of 1.25 million units, missing the 1.33 million median estimate by a wide margin. The slump was particularly severe in the multi-family sector, where structures with five or more units fell 26% to a five-month low. While single-family starts edged up 5.4% to an 874,000 pace, they remain near the bottom of a two-year range.

With the NAHB/Wells Fargo builder sentiment index languishing at a weak 39, the industry is increasingly reliant on concessions; 67% of builders reported using sales incentives in December to move inventory as buyers remain sidelined by affordability hurdles.

Bloomberg – US Housing Starts Fall to Lowest Level Since May 2020

______

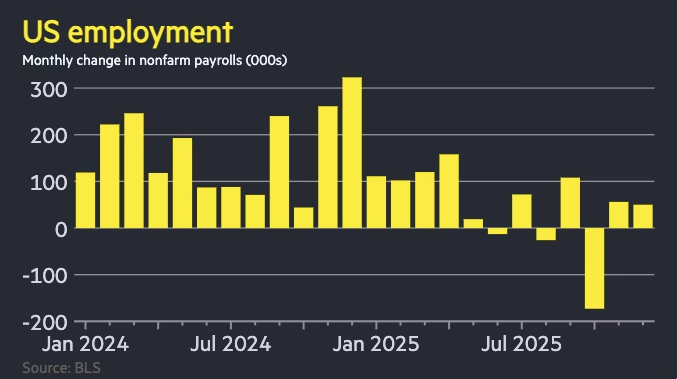

7. US Job Growth Slows to 50,000 in December; Unemployment Unexpectedly Dips to 4.4%

The U.S. economy added a modest 50,000 jobs in December, falling short of the 70,000 forecasted by economists, according to the Bureau of Labor Statistics. Despite the weak hiring figure, the unemployment rate unexpectedly dropped to 4.4% from November’s 4.6%. This latest report provides a much-needed clear view of the labor market following months of data distortion caused by the 43-day federal government shutdown last fall.

[Image showing US Treasury yield movements and Fed rate cut probability after December 2025 jobs report]

The December results capped off a “grim” 2025 for American workers, with average monthly job gains plummeting to 49,000 from 168,000 in the previous year. Following the release, short-term Treasury yields edged higher as the drop in the jobless rate dampened hopes for a January rate cut. Federal Reserve Chair Jerome Powell had previously expressed skepticism about BLS accuracy, suggesting actual job growth might be 60,000 lower per month than reported.

While hiring in the private sector remains in a “pause” as firms assess the impact of AI and trade policies, the surprise fall in unemployment has led major analysts, including those at Goldman Sachs, to predict that the Fed will hold rates steady at its upcoming meeting.

来源:Bloomberg – US economy undershoots expectations to add just 50,000 jobs in December

______